Press Room

Simvastatin - Supply Chain Reliability

CPhI 2003, 23 September 2003

Hovione for CPhI 2003

Cholesterol lowering agents (HMG CoA reductase inhibitors) recorded sales close to US$19 bil. in 2002 according to IMS Health figures. Atorvastatin from Pfizer and Simvastatin from Merck are the top two drugs of this therapeutic class, indeed they rank in the top two drugs in sales worldwide. They account for 71% of this market followed by Bristol-Myers Squibb’s Pravastatin. In the US alone the statins reached sales of nearly US$12 bil. in 2002 – well over one hundred tons of API.

The generic versions of Merck’s Zocor®, the second biggest product in worldwide sales, entered the German and UK markets last May, after Merck’s patent expired, rapidly achieving sales of about Euro 30 mil. in Germany in the first month alone (IMS Health). The performance of the generic versions of simvastatin in the first quarter after launch already suggested that the impact of the generic entry may not stay confined to this molecule, but might affect the overall statins class market. Indeed recent price pressures have seen growth in generic lovastatin prescriptions; which might indicate that generic simvastatin is likely to cannibalise some of the sales of Lipitor, if not even Zetia…

We are currently 2 years away from the simvastatin generic entry in the US, where approximately 40 tonnes of API were sold in 2002. Traditionally, after a US generic entry the volume of scripts more than doubles and the price more than halves. It should not come as a surprise that simvastatin might grow into a product of more than 100 tons of API. Capacity is very likely to be an enduring issue because simvastatin is technically difficult to make and the supplies of lovastatin limited.

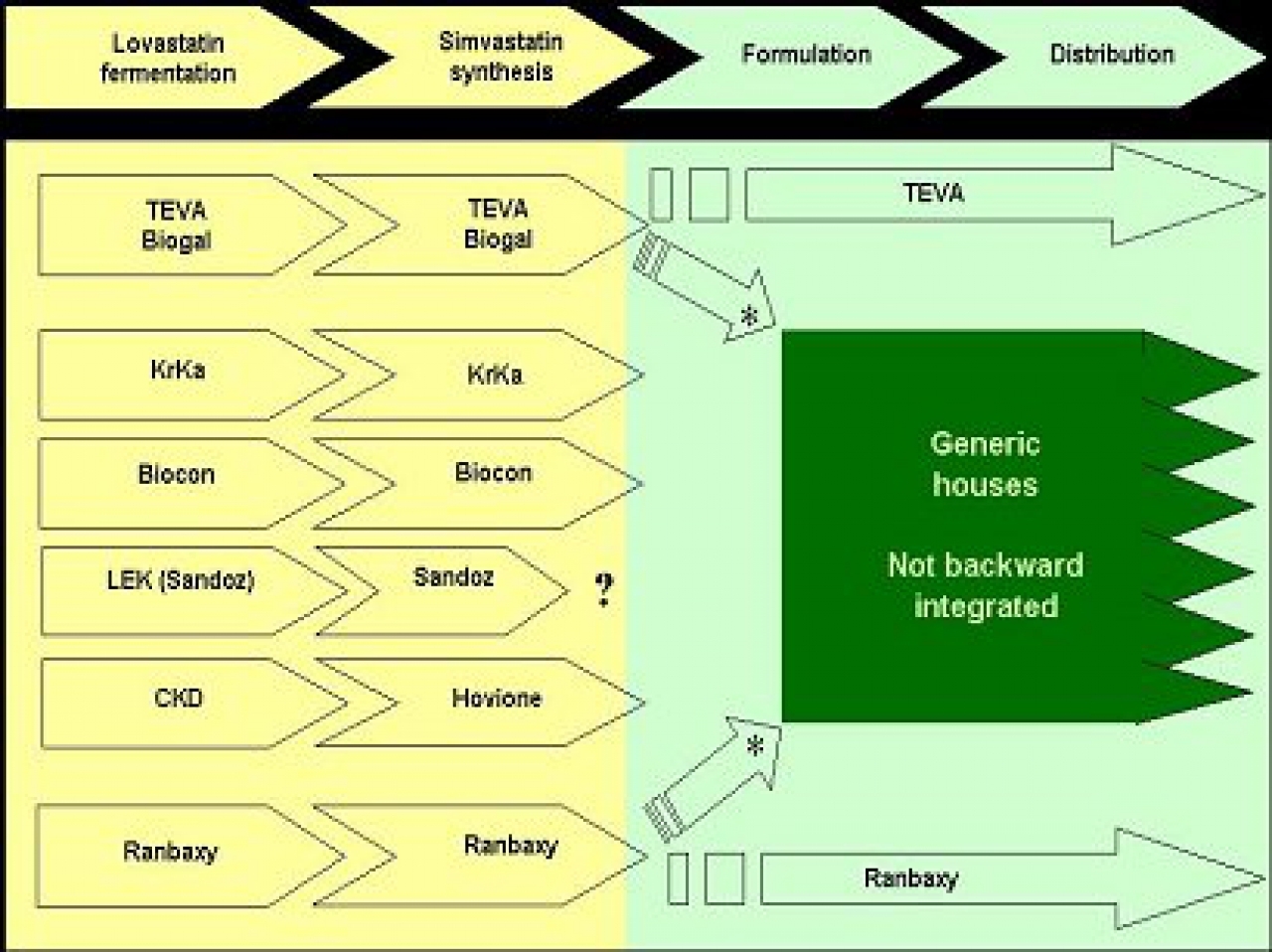

European pharmaceutical generic companies entered the market using registrations developed outside Europe by integrated houses able to make the API and the formulations. This is a normal course of action in Europe and enabled a very fast access to the market. As the quick entry focus looses ground to serving the market and expanding share – reliable supply will become a major concern.

The competitive landscape looks to us to be as follows:

* : The issue as to whether a supplier is a “partner or a competitor” is a very sensitive one. In the USA this is addressed earlier than Europe as most Generic firms usually develop their dossiers and source bulk. However given the high probability of a scenario of simvastatin API shortage it is very likely that an integrated player -both API producer and seller of formulations- will give preference to its own needs, to the detriment of supplying other generic firms.

Choosing the right API supplier has significant long-term impact.

Hovione is fully committed to supplying simvastatin bulk, and has no involvement in the dosage form business. This position, allied with a strong partnership with CKD that ensures the control and supply of the Lovastatin starting material, enables Hovione to present to customers a unique differentiation that guarantees a reliable supply of simvastatin API.